Many Long Island business owners treat tax season as a one-time event rather than an ongoing process. They gather documents in March, rush to file by April, and assume the job is done. This approach costs businesses real money every year. Missed deductions, IRS penalties, and poor cash flow decisions all trace back to last-minute filing habits. At Heritage Accountants & Advisors , we work with closely held businesses across Suffolk and Nassau counties to replace the rush-and-file cycle with a structured, year-round strategy.

Our tax preparation services in Long Island serve businesses across a wide range of industries, from trade contractors to healthcare providers to real estate professionals. What these businesses have in common is this: the ones that plan consistently pay less in tax and avoid the compliance risks that trip up last-minute filers. We have over four decades of combined experience helping Long Island businesses build proactive tax habits that protect their bottom line.

Disclaimer: This blog post is for informational purposes only and does not constitute tax or legal advice. Tax laws are complex and constantly changing. Please consult with a qualified tax professional regarding your specific business situation.

Last-minute filing costs businesses through penalties, lost deductions, and avoidable interest charges.

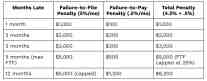

The IRS does not treat lateness lightly. Under IRS Topic No. 653 , the failure-to-file penalty runs at 5% of unpaid taxes for each month or partial month a return is late. This penalty caps at 25% of the total unpaid balance. A separate failure-to-pay penalty adds another 0.5% per month until the balance is settled.

If a return is more than 60 days late, the IRS imposes a minimum penalty. For returns due in 2025, that minimum is $510 or 100% of the tax owed, whichever is less. These charges compound quickly, and the IRS begins accruing interest on both the unpaid tax and any assessed penalties from the original due date.

Beyond penalties, rushed filings lead to documentation gaps. When business owners scramble to pull together records at the last minute, deductions get missed, and errors increase. Errors on tax forms are among the most common IRS audit triggers.

The table below shows how failure-to-file and failure-to-pay penalties accumulate for a business with $20,000 in unpaid tax at the time of filing.

Source: IRS Failure-to-File Penalty and Failure-to-Pay Penalty guidelines, IRS.gov

Note: When both penalties apply in the same month, the failure-to-file penalty is reduced by the failure-to-pay amount. Interest accrues separately on the unpaid balance and continues until paid in full.

Business tax deadlines depend on your entity type, and missing the wrong one triggers immediate penalties.

Many business owners assume their deadline is April 15. That date applies to sole proprietors and C corporations. Partnerships and S corporations face a March 15 deadline. Filing even one day late without an approved extension opens the door to penalty exposure.

The IRS offers extensions using Form 7004 for business entities. An extension moves the filing deadline, not the payment deadline. Taxes owed are still due by the original date. Heritage Accountants & Advisors helps clients determine the right filing dates for their entity structure and tracks quarterly estimated payments to avoid underpayment penalties throughout the year.

Under IRS guidance, individuals, including sole proprietors, partners, and many S corporation shareholders, generally must make quarterly estimated tax payments if they expect to owe $1,000 or more when they file. If they underpay or pay late, the IRS may assess an underpayment penalty, even if the annual return itself is filed on time.

Our business tax planning in Hauppauge, NY , prevents penalties by keeping financial records current and tax positions reviewed throughout the year.

Here is what proactive planning looks like in practice:

Quarterly reviews: We assess your income and deductions each quarter. This keeps estimated tax payments accurate and reduces the risk of a large underpayment at year-end.

Deduction tracking: Vehicle mileage, home office use, depreciation schedules, and retirement contributions all require documentation maintained throughout the year. Reconstructing these records in April is error-prone.

Entity review: As your revenue grows, your current business entity may no longer serve your tax interests. An S corporation election or restructuring decision has annual deadlines that cannot be made retroactively.

Capital expenditure timing: IRS Publication 946 allows businesses to deduct the cost of certain qualifying property through Section 179 and bonus depreciation. The timing, especially when the property is placed in service, affects which tax year the deduction applies to.

Heritage Accountants & Advisors builds these checkpoints into every client relationship. Business tax planning is not a seasonal conversation. It is a standing agenda item that affects every major financial decision your business makes.

Individual and corporate tax services address the full picture because business income and personal income are often deeply connected for closely held business owners.

For S corporation shareholders, partnership members, and sole proprietors, business income flows directly to personal returns. A decision made at the entity level changes the owner's personal tax liability. Without coordination between individual and business returns, deductions can be duplicated, lost, or misapplied.

This is especially relevant in New York, where state income tax rates add another layer of liability on top of federal obligations. New York City residents face additional surcharges that require separate planning. Heritage Accountants & Advisors provides individual and corporate tax services in NY , with both layers in view, so no opportunity is missed and no exposure is overlooked.

Rushed filings result in missed deductions that cannot be recovered after the return is submitted.

Business owners who wait until April to organize their records often leave money on the table. Some deductions require documentation maintained throughout the year. Others depend on decisions made before December 31. Once the tax year closes, these opportunities are gone.

Here are deductions that last-minute filers routinely miss:

Home office deduction: Requires year-round documentation of square footage and exclusive business use.

Vehicle and mileage expenses: IRS Publication 463 says mileage records should be kept at or near the time of travel. Reconstructed logs are weaker and may not be accepted without supporting evidence.

Retirement plan contributions: SEP-IRA and Solo 401(k) contribution windows close with the tax year. Late awareness means a lost deduction.

Qualified business income (QBI) deduction: Up to 20% of qualified business income may be deductible under Section 199A. Maximizing the deduction often benefits from mid-year planning.

Business meals: Business purpose must be documented at the time of the expense, not reconstructed later.

Heritage Accountants & Advisors works with our clients throughout the year to maintain the documentation each of these deductions requires. When tax season arrives, the work is already done.

New York State imposes additional tax obligations that many Long Island business owners do not fully account for until they are already behind.

New York is one of the higher tax-burden states for businesses and individuals. Beyond federal obligations, Long Island businesses must manage:

PTET election: Eligible partnerships and S corporations can elect New York PTET. It may create federal tax savings for qualifying owners.

Estimated tax payments: New York has its own quarterly estimated tax rules. Missing payments can lead to state penalties.

MCTMT: Some Long Island businesses may owe MCTMT. This can apply in Nassau and Suffolk counties.

Sales and use tax: New York sales tax rules are detailed. Errors or late filings can trigger penalties.

Heritage Accountants & Advisors tracks both federal and New York obligations for every client. Our team understands the layered compliance environment that Long Island businesses operate in. Waiting until April to review these obligations is too late to avoid penalties and too late to act on available elections.

CPA tax advisors provide value through proactive guidance, not just annual return preparation.

When evaluating an accounting firm, consider these factors:

Availability throughout the year: A firm that is only reachable in March and April cannot help you make good decisions in August.

Experience with your entity type: S corps, partnerships, and C corps each carry different filing requirements and planning opportunities.

Big Four or equivalent background: Advisors with large-firm training understand complex compliance environments and apply that knowledge to smaller business situations.

Familiarity with New York tax law: State-level rules around business income, pass-through entity taxes, and payroll compliance differ significantly from federal requirements.

The team at Heritage Accountants & Advisors carries Big Four experience into every client engagement. Philip Bellissimo, Managing Member, trained at PricewaterhouseCoopers before leading the firm through its January 2025 merger of BSB Associates and Ferrera, DeStefano & Caporusso. CPA tax advisors in Long Island with that background bring a level of depth that routine filing software cannot replicate.

When tax planning gets pushed to April, businesses often end up paying more than they should. Penalties, missed deductions, and cash flow strain are not just frustrating. They are often avoidable with the right planning in place.

At Heritage Accountants & Advisors, we help closely held businesses across Hauppauge, Long Island, and the greater New York metro area, including Manhattan and Brooklyn, stay ahead of tax obligations with proactive, year-round guidance. Our goal is to help you reduce surprises, protect cash flow, and make informed financial decisions before deadlines become problems.

Start the conversation before small tax issues turn into costly ones. To schedule your free consultation, contact us at (631) 543-7700 or info@heritage.cpa .